William Godsave of Credo, our wealth management partners, looks at how inflation is one of the key risks for those approaching retirement, and how you can plan for the future with inflation in mind.

Running out of money, stock market volatility, and rising care home costs are all common worries we hear from clients in retirement. Whilst these are of course important concerns, the risk rarely mentioned that will have a profound impact on all aspects of your financial planning, is inflation. So why do people not feel it in the same way as other risks and how can we deal with it in retirement?

Inflation: the silent risk

We recently met with a client to review their retirement plan. We first met her when she retired 5 years ago at the age of 56 and at the time, we undertook an analysis to assess the sustainability and trajectory of her retirement assets.

The outcome showed that she should have sufficient assets to meet her needs, but she would gradually eat into her capital, and may eventually be left with minimal liquid assets by her 90s.

During the most recent review meeting, our client said she believed our original modelling was wrong, because we had told her that her capital would be reducing over time when in fact the value of her portfolio was higher now than what it was five years ago. She even said that perhaps she should start increasing her expenditure or gift more to the children as she felt more financially comfortable.

The investment growth over the last five years had been slightly higher than originally assumed, but we had a feeling that this wasn’t the explanation. Going back to the original model, it turned out that it wasn’t the analysis that was wrong, but a lack of appreciation of how difficult it is for us to understand how inflation plays out in real life.

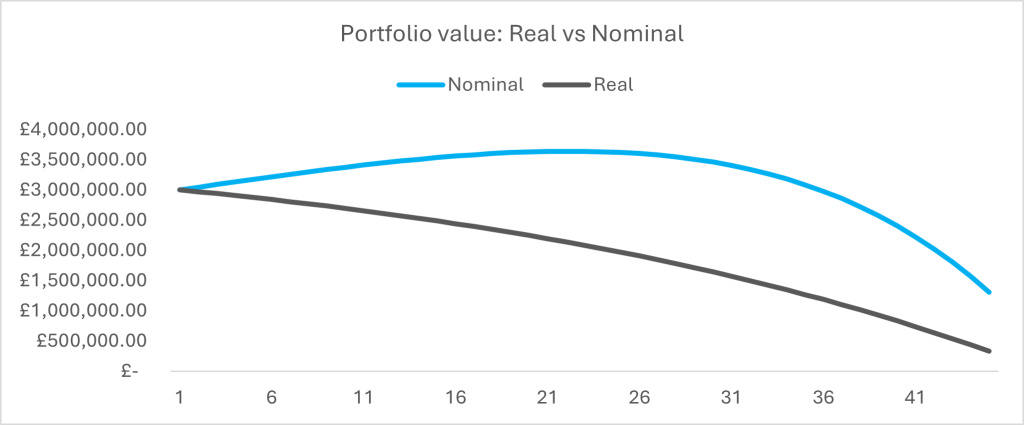

Let’s look at a simplified version of our client’s retirement plan to explain what was going on. The graph below is a basic projection of her assets over a 45-year period (i.e. her potential retirement period), assuming:

- Her portfolio has a starting value of £3,000,000 and grows by 5.5% per year (or 3% net of assumed inflation)

- She draws out £120,000 a year (so 4%) from the portfolio to meet her expenses, and the withdrawal amount increases with inflation at 2.5% per year.

The black line at the bottom, which is steadily going down, shows the value of our client’s assets in real terms (i.e. inflation adjusted to what the value is as at today), and is what we had been showing as her retirement path. However, in real life people don’t inflation-adjust the value of their assets; they normally anchor valuations to a certain point in time – for example the value at retirement – so the nominal value is really the journey that the client will see, as shown by the blue line at the top.

What this shows is that our client will see her assets increase in value for 25 years (relative to the starting value at retirement) before seeing a decline towards the end of retirement, when eventually the nominal value falls below the original £3m valuation.

That feels counter intuitive – if my assets are going up in value each year despite withdrawing an increasing level of income, how can I be at risk of asset depletion?

The reality is that our client’s portfolio will go down each year in inflation adjusted terms, it’s just that she didn’t know it as she, like most of us, was only thinking in nominal terms.

It may seem obvious now we’ve said it, but how many of us review our finances in real terms? I certainly don’t; when I see my pension increase by £20,000 over the last 12 months, I’m not thinking, well, that’s only a £7,300 increase in real terms.

Implications for planning and investing

The scenario outlined above is of course an oversimplification of reality, but nevertheless, it highlights an interesting characteristic of how inflation plays out in real life, and can affect a wide range of decisions, including:

- How much you can and should spend at different points in retirement

- How much you can afford to give away to beneficiaries during your lifetime, including when planning with structures (such as certain trusts or family companies), when you may be giving up the right to future growth or income

- Investment decisions around how much risk you should be taking and what return in real terms you need to achieve.

What can we do about it?

Have a financial plan that is underpinned by robust analysis

Whether it relates to your retirement or estate planning goals, ensure you have a plan which looks at both your short- and longer-term financial position and considers the impact of inflation (amongst other factors such as taxation and fees)

Review regularly

Update and refresh the plan on an annual basis or sooner if circumstances change or significant decisions need to be made, including reviewing assumptions and stress testing

Flexible spending

A certain level of flexibility with regards to spending may be needed to get you back on track or during periods of poor investment growth or high inflation

Investment strategy

Ensure you have a robust investment portfolio which considers the long-term real return of assets, and a strategy which is commensurate with your long term (inflation linked) needs.

Despite the clear importance of inflation in financial planning, we as advisers (let alone our clients) still struggle to fully appreciate its effect without going back to the inflation adjusted numbers. In a similar way to how compound returns are very difficult to comprehend without a spreadsheet, the human brain doesn’t seem to be wired to appreciate the impact of inflation over a long period of time either.

If you would like to discuss your retirement or investment planning, please do not hesitate to reach out to us at credo@pkf-l.com.

Important Notice

This marketing material has been prepared and issued in the United Kingdom by Credo Capital Limited (“Credo”). It is provided to you for discussion purposes only and does not constitute and should not be interpreted as either investment advice (including legal, tax or accounting advice) or a trading recommendation. This marketing material is not a solicitation to buy or sell any financial instruments or commodities, a recommendation to participate in a particular trading strategy or to invest into regulated or unregulated funds. The value of an investment can fall as well as rise and is not guaranteed, your capital may be at risk and you may not receive back your original investment in full.

Credo Capital Limited is a company registered in England and Wales, Company No: 03681529, whose registered office is 8-12 York Gate, 100 Marylebone Road, London, NW1 5DX. Authorised and regulated by the Financial Conduct Authority (FRN:192204). © 2024. Credo Capital Limited. All rights reserved.