The UK insurance broking sector has continued to evolve over the past 12 months, shaped by a combination of market dynamics, political uncertainty and changing economic conditions. We examine the impact of these developments and assess the potential for a soft market in insurance rates. We provided analysis for Insurance Age’s flagship annual ‘Top 100 Brokers’ survey.

Transactions and market confidence

Overall, confidence in the insurance broking sector remains high and the consolidation of the market has continued apace. Transactions have been buoyed by a combination of robust demand for insurance services and attractive valuations. M&A activity at the smaller end of the market has remained buoyant. Appetite for mid-to-larger transactions, which had seen a drop last year, rebounded in 2024, with deals involving DRP and SRG being particularly notable.

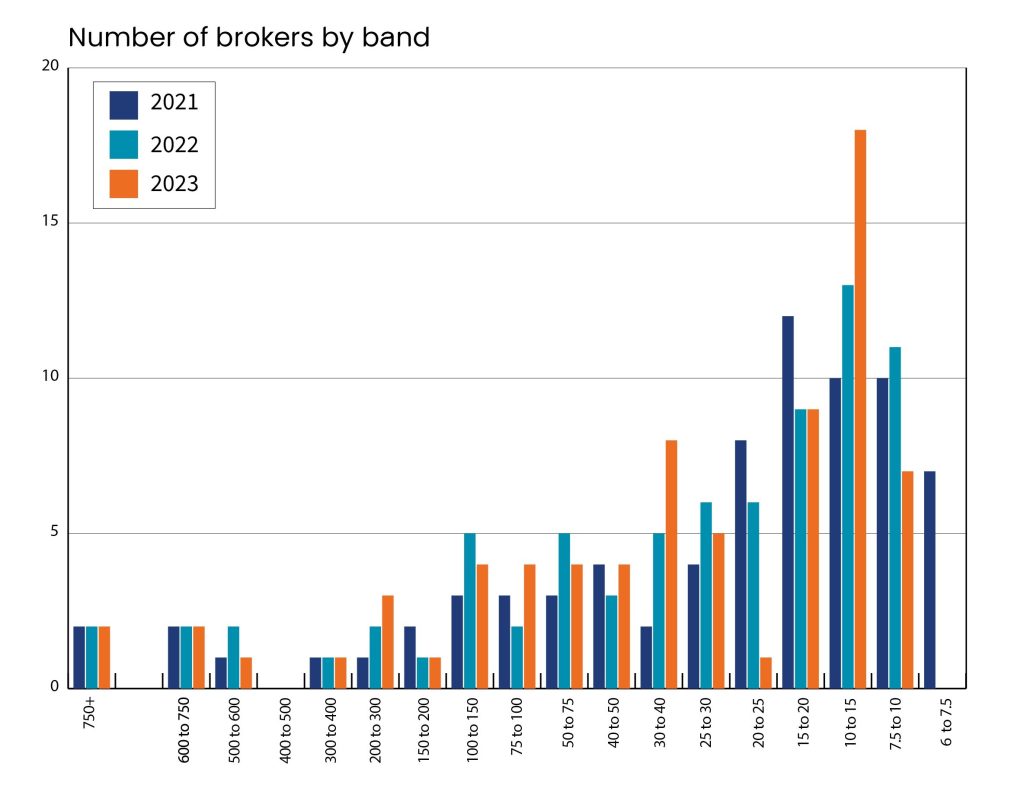

This ongoing consolidation – together with the favourable hard market conditions – has meant that the total size of the market for the Insurance Age broker universe has grown by nearly £1 billion per year over the last few years and the minimum size needed to qualify has also increased.

The multiples achieved by larger intermediaries continue to attract premium rates. Valuations can be influenced by several factors, including the quality of the brokerage’s client base, either a unique specialism or a diverse offering, and its technological capabilities.

Brokers that have invested in digital transformation and data analytics have the potential to improve value by enhancing operational efficiency and client engagement. In particular, management teams that have been able to show their success with improved data analytics have enjoyed a less challenging due diligence process!

High interest rates do not appear to have deterred activity; insurance brokers have been relatively good at finding ways to finance their acquisitions. As interest rates stabilise, we do not anticipate significant changes in this regard. However, some brokers may look to refinance their debts if their terms can be improved to enhance returns.

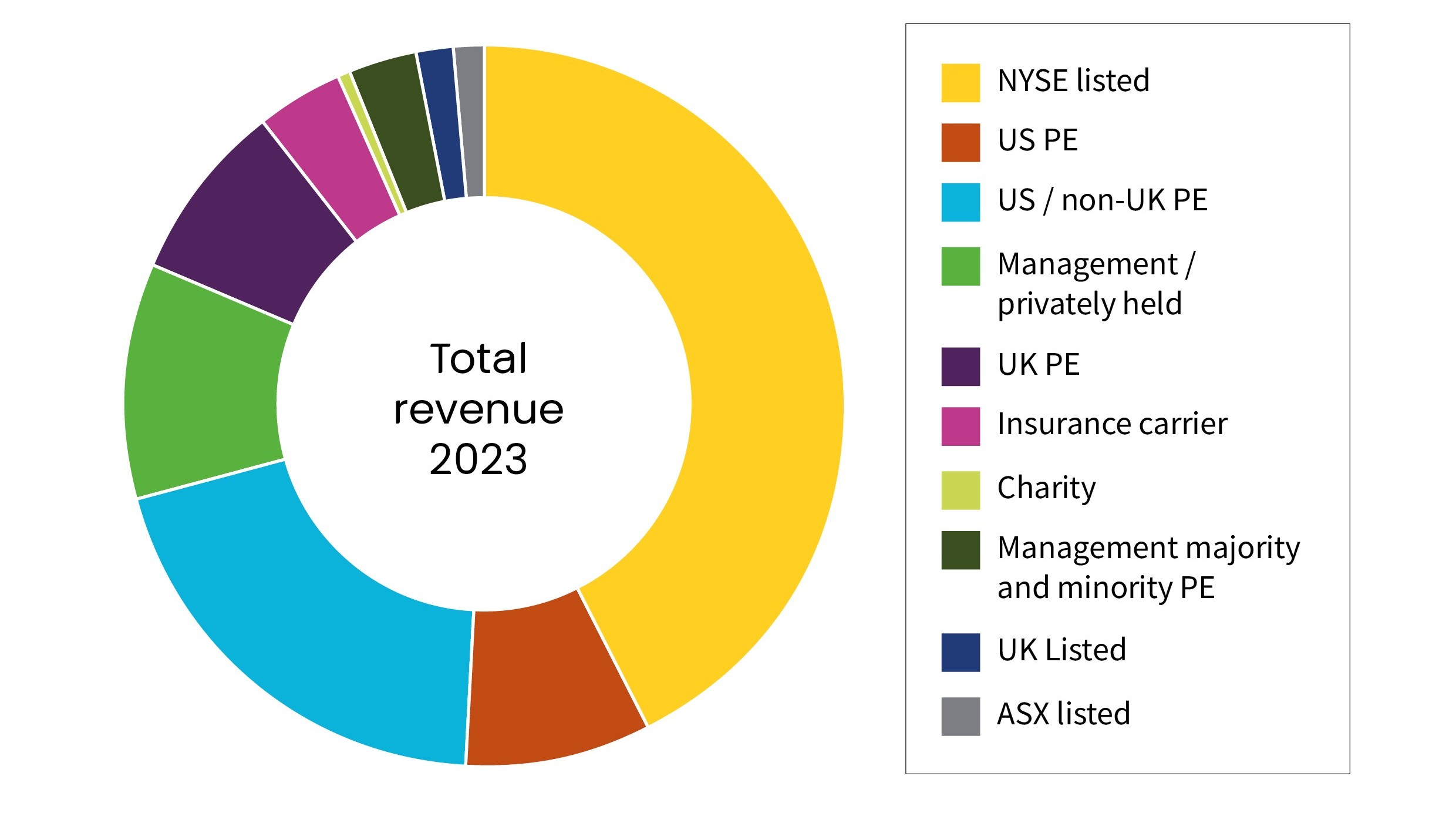

Overall, the 2024 market remained dominated by listed large brokers and private equity-backed (PE) businesses, which make up over 80% of the universe by value.

Expansion into Europe and Australia

UK consolidators are increasingly looking beyond domestic borders, with Europe and Australia being particularly prominent at the moment. Both private equity firms and consolidators are eyeing these regions, attracted by the potential for consolidation in markets that are not yet as saturated as the UK.

In Europe, the insurance broking landscape varies significantly from country to country, offering a mix of opportunities and challenges. Consolidators are focusing on markets with fragmented broker networks, where there is room for consolidation and efficiency gains. Similarly, Australia presents a promising market, with growing demand for insurance offerings coupled with a relatively low market concentration.

The political environment and its implications

The Labour government is already having an impact on the sector. One of the most pressing political concerns is the potential for increases in Capital Gains Tax in last October’s Budget. This is already leading to a push to finalise acquisitions as quickly as possible. Indeed, we have seen the volume of transactions picking up recently in response to growing media speculation about imminent tax rises and the mood music from Downing Street.

Looking ahead, the future political landscape remains uncertain. While Labour has been at pains to paint themselves as pro-business, broker management teams will need more clarity if they are to successfully navigate any shifts in regulatory and economic policies.

The prospect of a soft market

The sector is currently facing the possibility of entering a soft market phase, characterised by lower premiums, increased competition and more favourable terms for policyholders. Several factors are contributing to this potential shift.

Interest rates have been on a downward trend, with lower investment returns potentially leading to a more competitive pricing environment as insurers seek to maintain their market share. Additionally, inflation has shown signs of stabilising at a lower level, which can influence the cost of claims and, consequently, insurance premiums. On top of this, we have seen the launch of more MGA start-ups, which are looking for market share and may be pushed to price competitively to gain traction.

This combination of factors could tempt brokers to try to secure better terms for their clients after years of rate increases. This may then act as a drag on organic growth, as rate changes have been a key driver for some broking businesses in recent years.

This is by no means a certainty, however. Lloyd’s, which has been focused on improving the profitability of its syndicates, has been advising caution about the impact of the soft market and urging everyone to hold strong. The market will wait to see how these competing factors play out over the coming year.

Final thoughts

The UK insurance broking sector continues to navigate the evolving landscape – as it always has done! Mid to lower-market transactions continue to thrive, driven by strong market confidence and attractive valuations. UK consolidators are continuing to expand their horizons, exploring opportunities in Europe and Australia to capitalise on less mature markets. The political environment remains a key consideration, with potential changes in CGT and uncertainty about the new government’s approach to business influencing strategic decisions.